Several accounting changes have taken place in the last few years for states to show more transparency in how they report their pension debt.States used a very misleading discount rate method of 7.5%. If you were a business using this same method, you’d be investigated by IRS and your accountants probably wouldn’t even do it. The GASB issued accounting guidelines for change in 2012 and now the new data is rolling out.

For Indiana (graphs below), without boring the audience to death, the new accounting methods are applied and the state pension funding ratio drops dramatically. The pension fund “unfunded liabilities” jumped to over $60 Billion. A $4 Billion increase from the year before.

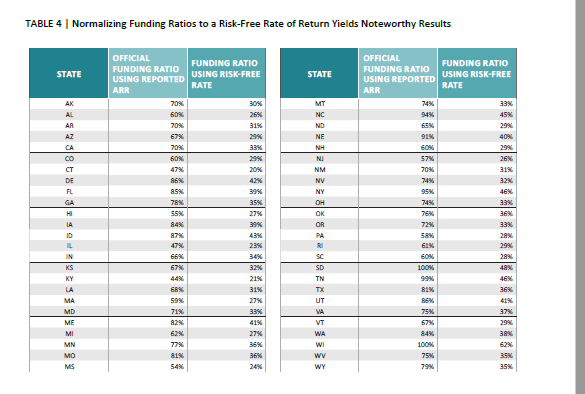

Here’s more from ValueWalk.com:

Recently, the American Legislative Exchange Council (ALEC) has produced a report that is nothing short of alarming. The report suggests that the 7.5% discount rate utilized by many pension systems is nothing more than a flight into wishful thinking. When a realistic discount rate, such as the risk-free rate, is utilized the state’s pension system appears to be unconscionably unstable. The report entitled “unaccountable and unaffordable” exclaims, “Faulty accounting and reporting methods obscure the magnitude of unfunded liabilities.”